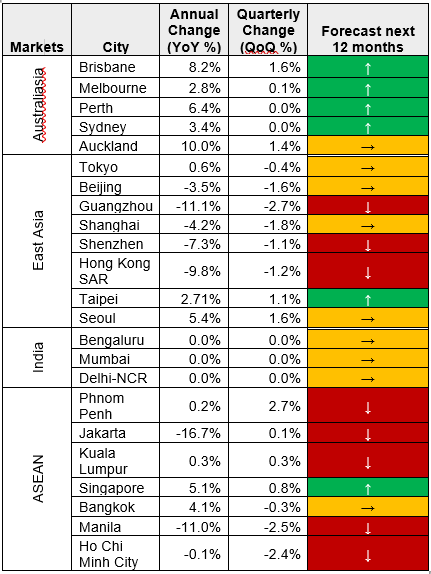

SINGAPORE (October 20, 2023) – In their Asia-Pacific Prime Office Rental Index for Q3 of 2023, Independent global property consultancy Knight Frank points out that the declining property rental rates have moderated, in addition to the markets of the Chinese mainland also showing moderation.

However, this moderation was counter-balanced by a growth in rentals in other developed markets. The report, published on a quarterly basis, shows that in line with Q2 of 2023, a majority of the cities under observation (i.e. 15 out of 23) show either a stabilisation or an increase in rents.

Despite this stability, vacancies continue to rise by 0.4% on a quarter-on-quarter basis to 14.4%.

Tim Armstrong, global head of occupier strategy and solutions said: “Despite vacancies rising in the region, rental declines in the third quarter have stabilised, supported by a trend favouring flight-to-quality properties. Overall, the current expansionary cycle in the region affords occupiers a broader range of options and strategies to consider, enhancing their ability to secure favourable lease terms amid current soft conditions. While it is still premature to make a definitive judgement amidst the most recent political developments, the evolving geopolitical landscape is expected to cast a shadow on occupier prospects as companies meticulously evaluate the accompanying risks. As businesses adapt to a future hybrid work model, the trio of location, amenities, and sustainability have gained significance in rebalancing the scales in favour of in-person work.”

Christine Li, head of research, Asia-Pacific said: “Vacancies rose despite a notably subdued completion pipeline of just over a million square meters in the quarter, marking a steep decline of approximately 75% from Q2 2023, as absorption trails behind the rate of new constructions in the region. Monetary tightening, inflationary pressures and geopolitical events continue to weigh on economic sentiment, as occupiers remained cautious, taking longer to consider space requirements. The backdrop of monetary tightening, inflationary pressures, and ongoing geopolitical events cast a shadow on economic sentiment, resulting in occupiers exercising caution and taking extended time to evaluate their space requirements.”

With the growing popularity of hybrid work schedules, occupier strategies have separated from considering only headcount. In fact, according to Knight Frank’s (Y)OUR SPACE 2023, more than half of the occupiers surveyed believe that their organisations will embrace hybrid work styles in the next three years.

Ms Li adds, “This will continue to place emphasis on space optimisation strategies. Evolving strategies will likely dampen leasing velocity for the rest of the year, even as macroeconomic volatility hampers occupier ambitions. Consequently, market conditions across most of the region will continue to favour tenants into the initial stages of 2024.”